The Iran-US war, now in its seventh week, has turned from a distant headline into the single biggest threat to the 2026 Cyprus tourism season. Arrivals fell roughly 30% in March, hoteliers are reporting a 40% slump in March and April bookings, and the pace of new reservations has not recovered. A drone strike on the British base at Akrotiri in March pushed the United States to lift its Cyprus travel advisory to Level 3 — "Reconsider Travel" — and the ripple effects are showing up in every channel manager on the island.

As President of the Cyprus Short Term Rental Association, I hear the same questions from operators every day: Will guests cancel? Should I cut rates? Should I open for winter instead and ride this out? This piece answers them with what we know right now, what we can reasonably plan for, and what I would do if I were running a property today.

Where the war stands today

As of mid-April 2026, the US-led blockade of Iranian ports is in force after peace talks in Islamabad failed to reach agreement. A ceasefire between Israel and Hezbollah began in Lebanon on 17 April, and the White House has signalled a second round of negotiations within days, with President Trump calling a deal "very close". The sticking point is the duration of any uranium enrichment freeze: the US is pushing for twenty years, Iran has offered five.

Two things matter for operators. First, nothing has been signed. The current calm is fragile and could reverse on a single incident. Second, even if a ceasefire holds from here, the booking damage done over the last seven weeks does not unwind overnight — guest confidence takes months to rebuild, not days.

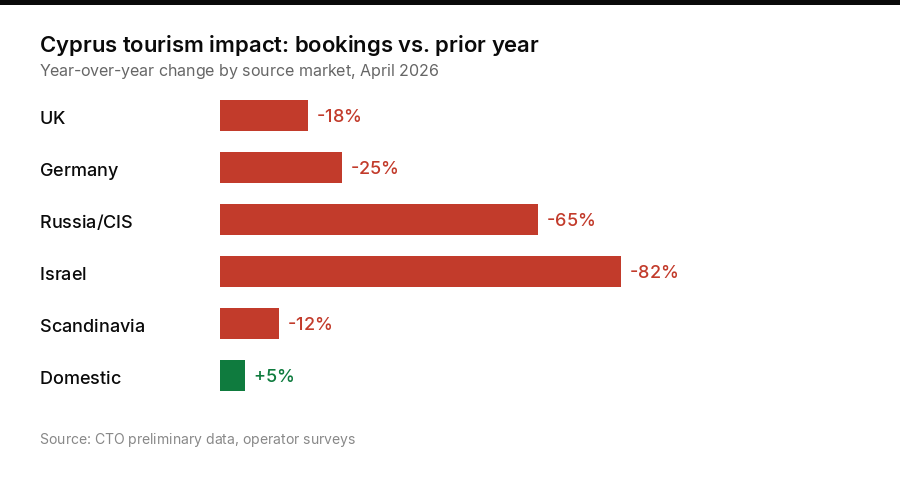

The numbers hitting Cyprus

The topline figures published by the Cyprus Mail and regional travel outlets are sobering. Tourist arrivals to Cyprus dropped about 30% in March 2026 versus March 2025. Hotel bookings for March and April are reportedly down 40%, and pace for May is tracking well below last year. Some industry voices are modelling a 40% full-season booking dive if tensions hold.

Demand has not disappeared from Europe — it has rotated. Reuters data shows Spain flight bookings up 32% year on year, Spanish hotel searches up 28%, Portugal flight bookings up 21%, and Portuguese hotel searches up 16%. Northern European travellers who would normally book Cyprus, Greek islands, and parts of the Aegean are choosing the western Mediterranean instead.

What this means in practice

If you budgeted for a flat-to-growth 2026 season, you are probably 25–35% behind pace. Do not wait for May to revise. Rebuild your forecast now using the last four weeks of actual booking data, not last year's pace.

Why Cyprus is more exposed than Spain or Portugal

Three specific factors are weighing on Cyprus more heavily than on the western Mediterranean. The first is geography. Cyprus sits roughly 100 km south of Turkey and about 400 km from the Levantine coast. Guests looking at a map do not calculate that this is still further from Tehran than Rome is from Warsaw — they see proximity and they defer.

The second is the Akrotiri incident. A drone strike on an active British sovereign base on Cypriot soil is an extraordinarily rare event, and it was heavily covered in UK and US media. The United States moved its Cyprus advisory to Level 3 shortly after. Germany, France and other key source markets have issued softer caution language, but the directional signal is the same.

The third is air connectivity. Many Cyprus routes share infrastructure and overflight corridors with flights that transit the Middle East. When airlines reroute to avoid the Strait of Hormuz or contested airspace, capacity and fares to Larnaca and Paphos move against us. Spain and Portugal face none of that.

Pricing in a demand shock

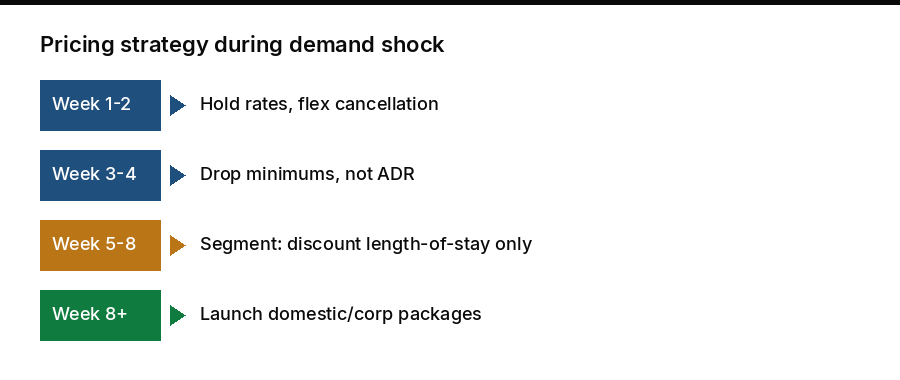

The instinct in every revenue meeting right now is to cut rate. In most cases I would push back against that — at least not as the first lever.

Demand that has paused for safety reasons does not come back because rate dropped 15%. A traveller who took Cyprus off the list because of the US advisory does not put it back on because you are 15% cheaper than last year. You have given away margin without moving the booking curve. Discounting works for price-sensitive demand, not for fear-sensitive demand.

What I would do instead, in rough priority order:

- Protect ADR on your base weeks (July and August). Summer school-holiday demand from the UK and Germany is the most resilient segment. Hold rate there.

- Open flexible-rate inventory for May and June at a modest discount to 2025 with clear free-cancellation terms. This captures late-booking behaviour as the news cycle calms.

- Build value, not discounts. Add a third night free, a paid-for transfer, or a dining credit. These cost you less than a rate cut on paper and preserve your reference price for 2027.

- Cut rate last, and selectively. If you have to discount, do it on softer weeks and softer room types, not across the board.

Cancellations and guest trust

Operators are reporting elevated cancellation rates on non-refundable bookings as guests push for goodwill refunds. How you handle this in April and May will define your review scores and repeat-guest economics for the next two years.

My guidance to CSTRA members is simple. Inside 14 days of arrival, honour your stated policy. Beyond 14 days, offer a date change at no cost up to 12 months, even if the guest booked non-refundable. The cost of a rebooked stay in October is far lower than a one-star review that says you kept a family's money during a war scare.

On communication: a short, factual message to every guest arriving in the next 60 days goes a long way. Acknowledge the situation, state that your property is operating normally, summarise what local authorities are saying, and provide a named contact. Generic reassurance reads as PR. Specifics read as competence.

Diversifying your demand mix

This crisis is exposing how concentrated some Cyprus operators are on two or three source markets and one or two OTA channels. The operators I see coping best are the ones with a diversified book of business before the war started.

Three segments still have demand worth chasing in the next sixty days:

- Domestic and regional short-haul. Cypriot residents, Greeks, and nearby Gulf travellers are closer to the news and less panicked than distant source markets. Promote short-break packages with local language copy.

- Long-stay and remote workers. The "monthly apartment" demand for Cyprus has not evaporated to the same degree as seven-night family holidays. Open 28-plus night rates on Airbnb and Booking.com, and push them on your direct channel.

- Corporate and project-based stays. Contractors, film production, and research bookings are largely insensitive to headlines once contracts are signed. This is a good time to revisit your corporate rate file and make outbound calls.

If you are 70% dependent on one OTA and two source markets in a normal year, this is the wake-up call to fix that. Our piece on direct bookings for Cyprus hotels and STRs lays out a 90-day plan for doing exactly that.

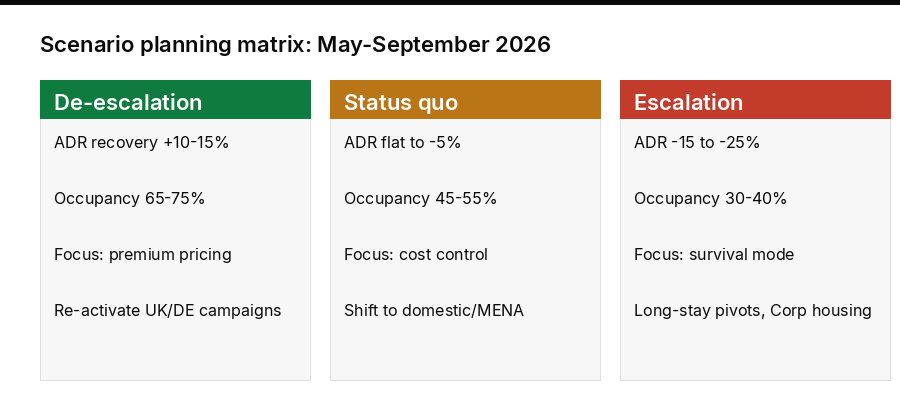

Scenario planning for May through September

I am running three planning scenarios for operators I advise, and I suggest you do the same.

Scenario A — Rapid de-escalation (probability: moderate). A framework deal is announced within two to four weeks, the blockade is lifted, and travel advisories ease through May. Bookings recover on a lag, with May still down 25–30%, June down 10–15%, and July onward close to plan. Full-year revenue lands 10–15% below budget.

Scenario B — Protracted standoff (probability: moderate). Talks continue without a deal, the blockade holds, and no further escalatory incidents occur. Travel advisories stay in place but do not tighten. Cyprus season lands 25–35% below 2025 for the full year. This is the scenario to budget against today.

Scenario C — Re-escalation (probability: lower, but consequential). A kinetic event in the Eastern Mediterranean or a collapse in talks pushes advisories higher and triggers airline capacity cuts. Cyprus season lands 50%-plus below plan. Cash conservation, not growth, becomes the priority.

Run each scenario through your P&L. Identify the month where Scenario C breaks your covenant, overdraft, or personal liquidity, and pre-plan the lever you would pull — staff flex, supplier terms, owner drawdown — before you need it.

The upside if de-escalation holds

Cyprus has been through regional shocks before — 1974, 2006, 2013, 2020 — and the pattern is consistent: once the news cycle turns, recovery is sharper than anyone predicts during the crisis. Deferred travel stacks up, airlines reposition capacity, and the value proposition of a safe, English-speaking, EU-member island in the Mediterranean reasserts itself quickly.

The operators who come out of 2026 strongest will be the ones who protected rate where they could, handled guests with grace when they could not, and used the downtime to fix the parts of their business they had been putting off — the listing that needed rewriting, the direct-booking engine they never set up, the corporate accounts they never chased. The war is not something any of us can control. Everything else on that list, we can.

Need help rebuilding your 2026 plan?

I'm working with Cyprus hotel and STR operators on revised-pace forecasting, rate strategy, and demand-mix diversification for the back half of 2026. Book a consultation and we'll stress-test your numbers against the three scenarios above.

Schedule a ConsultationSources

- CNN — US military blockade on Iranian ports takes effect (13 April 2026)

- Al Jazeera — Lebanon ceasefire begins; Trump says Tehran deal close (17 April 2026)

- Cyprus Mail — Tourist arrivals to Cyprus drop 30 per cent (15 April 2026)

- Cyprus Mail — Tourism sector hopes for regional calm (16 April 2026)

- Euronews — Cyprus war-related tourism concerns (26 March 2026)

- Euronews — Iran conflict costs Middle East travel €515 million a day (11 March 2026)

- Oxford Economics — Tourism impacts in the Middle East from the Iran war